Hi. Good morning. How are you? I’m excited this week to bring you a much more in-depth analysis of the Roth Conversion Ladder, a method used to spend retirement money early without penalty and with little to no tax burden. I’ve already talked about this method here, here, and here, but I decided this very important topic needed its own special post.

Changing subjects momentarily, I get a real kick out of directly translating ridiculous American expressions in other languages. For instance, when in a German grocery store in 2018, I suddenly wondered if German lovers addressed each other as honig, the German word for honey.

Honig! I’m home!

See, isn’t that fun?

This week we will investigate the intricate web of methods designed to spend the money you’ve saved. It’s not all milch und honig.

Listen in Podcast Form

Step 1: How much does your life cost?

I’ve been banging the table for years on this. Whether you are saving for a trip, an early retirement, a few pounds of fine French truffles, or an $80 pair of new/old ripped jeans, it’s quite wise to track your spending. In absence of full-on tracking, we all need to have a solid idea of our expected yearly spending—and how that might change.

A year or two ago, I was dialed in tight like my psoas on what we planned to spend on any given year. Given that we’ve sold a home, moved to a new state, bought another home, left employer-sponsored health insurance for marketplace insurance, lived on the road for five months, and all kinds of other major life changes, I’m feeling slightly less certain on our spending expectations.

We now have a range of expected yearly spending between $30,000 – $50,000 per year (with upward room to spare). I know, that seems super unrefined—and it is—but we were intentional not to limit ourselves to an upper end that felt restrictive or limiting. I mean, I don’t want to have to check the budget to see if I can afford a candy ring*. My guess is that we’ll end up somewhere much closer to the lower end. After all, self-denial, right?

*Fun fact: Mrs. CC and I were engaged with a candy ring. Shocking, perhaps. I even bought two of them from a fancy Manhattan custom candy company and smuggled them to Texas like fine Columbian cocaine. We ate the engagement ring immediately, and we froze the backup. It died tragically seven years later, along with an eight-week supply of meat, when our fridge quit on the job while we were out of town. We used all that ridiculous metal “symbology” money to travel to Thailand and make real memories instead. YMMV.

Step 2: Taxes and the Roth Conversion

What is the difference between a taxidermist and a tax collector? The taxidermist takes only your skin.

Mark Twain

Taxes, after all, are dues that we pay for the privileges of membership in any organized society.

Franklin D. Roosevelt

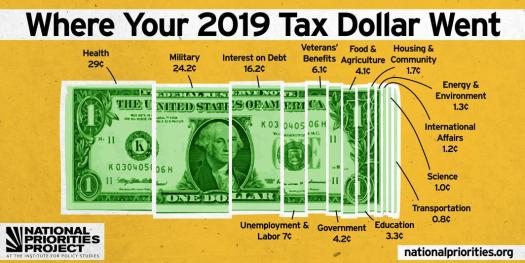

Ah yes, taxes. This is a potentially sticky subject. Here’s the skinny: I’m looking to minimize my tax obligation, through very legal and morally sound ways. Is it wrong to minimize taxes? It is if you do so illegally. That said, looking at our 2020 returns, we paid a lot of taxes. I mean, a lot. And all the years prior to 2020 for the last decade…a lot of taxes.

Yes, we made good salaries in our career. The downside is that we floated for years in the rough waters of high tax bracket seas, paying a much higher percentage of our income towards taxes.

I, for one, am all for responsible government spending, taking the side of Frankie D above. That said, there’s no getting around a simple fact: if you make less money, you pay less taxes. We now choose to make less money.

Here’s how we choose to manage taxes:

The Roth Vs Traditional 401(k) Debate

Early in my career, deep in the south Texas swelter, I received a mass email from the company HR department with the exciting news that we were now being offered Roth and traditional 401(k) contribution options.

And I’m like, “Who’s Ruth?”

Like a well-trained millennial, I turned to my trusted mentor: Google.

There I learned the following:

Traditional 401(k) contributions are not taxed when contributed, but will be taxed when withdrawn. Ideally by the time of withdrawal, the retiree will be in a much lower tax bracket. All traditional 401(k) contributions are tax-deductible in the year of contribution.

Roth 401(k) contributions are taxed now, at your current tax bracket, but will be left to grow and can later be withdrawn tax-free. In other words, the employee takes the tax hit now (at a higher tax bracket), but will not have to sweat any tax burden in the golden years. Roth contributions are not tax-deductible.

Because understanding taxes felt like reading Greek at the time, I opted to do a 50/50 split. There was no strategy. Both sounded good, so I figured I’d take a scoop of chocolate and a scoop of vanilla. A little chicken, a little beef. Surf and turf, yummmm.

The Roth Conversion Ladder

Fast-forward a few years and I discover the Roth Conversion Ladder. The Roth Conversion Ladder allows for us to (legally, morally, ethically, justly) move traditional retirement contributions—which were not taxed when contributed—to a Roth IRA, where those same funds will continue to grow and then can be subsequently withdrawn tax-free!

The Roth Conversion Ladder allows us to, in theory, build a (federal) tax-free retirement nest egg.

Who can do this? Early retirees or anyone with income in a low tax bracket.

Now, you know I loathe the term “retiree” for someone my age. I don’t identify with the image it conjures up, but I certainly enjoy the financial gifts this ultimate life hack provides.

The reason a Roth Conversion is possible for us is because we’ve suddenly dropped from a high to low tax bracket environment. Why is being in a low tax bracket important? A Roth Conversion is a taxable event, so going through this rigmarole in a high tax bracket will defeat the intended purpose of paying less taxes. But let’s not get ahead of ourselves.

Here’s how to swing with the hips and execute a proper Roth Conversion:

Step 0: Save and Invest. Consider current income and tax bracket.

Save your money and invest it, starting with employer-sponsored retirement plans.

If current income is in the 22% (or higher) tax bracket, a contributor should focus on traditional (non-Roth) contributions to a retirement account during the working years. If income is in the 10-12% tax bracket, then I’d maybe consider going harder on Roth 401(k) contributions, if available. As income rises, shift more focus towards traditional, pre-tax contributions.

Remember though, Roth contributions are not tax-deductible. Because the government only gives us one chance to lower our tax obligation in the year we are paid, it has always made more sense to me to maximize my traditional contributions. By doing so I make a tax-free contribution to my retirement AND lower my tax obligation in the current year. Even in a lower tax bracket I might still go 80%+ traditional.

There’s plenty of debate on the subject of traditional vs Roth, but I’d argue that we’re potentially missing the forest for the trees. Are you maxing out a retirement plan? Ok, fantastic! Let’s not sweat the details too much.

(Related Post: The CC Family Investing Strategy, Part 1: Philosophy and Asset Allocation)

(Related Post: The CC Family Investing Strategy, Part 2: Where Exactly Is Our Money?)

Step 1: Retire or otherwise quit your job.

Before initiating a Roth Conversion, wait until you enter a calendar year with little or no W-2 income (i.e., make a nice little nest in the 10-12% tax bracket habitat).

Step 2: Convert your 401(k) to an IRA.

Complete this step as soon as you leave your job, unless you have contributed to a Roth IRA (backdoor or otherwise). In which case, wait until January of the following year. Traditional contributions will be converted to a—you guessed it—traditional IRA. Roth contributions will be transferred to an existing Roth IRA, or one will be created.

We use Vanguard, and here’s their simple process.

Step 3: Move funds from a Traditional IRA to a Roth IRA (Roth Conversion)

This is the Roth Conversion. Don’t do this in a year with lots of other W-2 income (see Step 1 above).

**Important note: funds transferred during a Roth Conversion are 100% taxable as ordinary income.

So, if you decide to transfer all $400,000 of your 401(k), that’s going to hurt! This is something we are going to do little by little for many years. As a general rule of thumb, aim to convert about one year’s worth of living expenses.

Step 4: Let each contribution “season” for five years.

To withdraw Roth conversions without penalty or tax, you must sit and solve tax riddles for five years while your funds emerge from their Roth cocoon and can be spent like the beautiful and majestic butterfly they are. Earnings will be subject to tax and penalty for those under the age of 59 1/2. Make sense?

Step 5: Spend (federal) tax-free dollars.

Note: The amount of the original conversion, but not earnings, can be withdrawn penalty- and tax-free before the age of 59 1/2, so long as those contributions have seasoned for five years. After age 59 1/2, seasoned conversions and earnings can be withdrawn without tax or penalty.

How Much Should I Convert Each Year?

The standard advice is to do a Roth Conversion roughly equal to yearly spending. If we plan to spend around $40,000 per year, we’d want to convert $40,000 each year, wait five years, and then spend that tax- and penalty-free money.

The problem is that we are going to owe taxes on a portion of this $40,000. While minimal, paying taxes to not pay taxes seems like a bit of a head-scratcher.

Here’s how this works for a couple that’s married and filing jointly.

Yearly Expected Spending = $40,000

Anticipated Roth Conversion = $40,000 (considered as ordinary income by IRS in the conversion year)

(minus)

Standard Deduction in 2021 = $25,100 (deducted from ordinary income)

Taxable Income = $14,900

If we convert $40,000 in 2021, we will have a taxable income of $14,900, landing us squarely in the 10% tax bracket. Easy math there, we’ll owe $1,490 in taxes. Certainly, being taxed at 10% on a very low total income is better than being taxed at a higher bracket with a much higher income. So, we’re still winning, my friend.

What’s surprised me in the last year though is that none of the FIRE bloggers seem to talk much about budgeting for taxes. Obviously, the way to spend zero on federal taxes is to convert the amount of the standard deduction plus any other tax deductions possible, which include HSA contributions. Otherwise, federal and state taxes must be a part of the budget.

Should I Convert More?

Maybe.

We are working within the tax code as it stands today. If anything, I’m betting on higher (not lower) future taxes. Perhaps it’s best to fill the 12% bracket and pay a known tax now instead of an unknown (and probably higher) tax in future years?

I’d agree, but here’s one complication: Healthcare

I’ve already written about this complication at length, particularly in this post, so I’d suggest reading that one first. Basically, by maximizing our Roth Conversion we could be incurring higher healthcare costs, negating our “tax” efficiency. It’s a complicated game, so that’s why we are landing somewhere in the middle.

Our Roth Conversion Plan

We are likely going to convert $40,000 per year at year-end, once the dust settles on our full income situation. We don’t have any plans for traditional W-2 income yet, but we need to weigh the impact of dividend and any other unforeseen income.

Our total income will probably be in the range of $60,000. This is the figure we reported for our healthcare premiums when we changed to a Bronze plan with the new and exciting ARPA healthcare changes. At most, we will have a total taxable income of $35,000 ($60,000 – standard deduction of $25,100), which would require us to pay right around $4,000 in combined federal and state taxes. Because a good chunk of this will be qualified dividend income, we’ll probably only owe about $2,000 in taxes. So, somewhere between $2,000 – $4,000 in total tax burden. Not bad.

How Do You Fund Your Life Until A Roth Conversion “Seasons”?

For anyone retiring early or otherwise enjoying an extended time without traditional income, there are four options to bridge the five-year “seasoning gap” in absence of earned income.

1. Save five years of cash.

This is not ideal. Large sums of cash, while offering a sense of security, in fact carry risk. These funds are not outpacing inflation in the market.

2. Contribute to a Roth IRA or Roth 401(k) during working years.

Any previously-seasoned Roth contributions (but not earnings) are 100% tax- and penalty-free. However, consider whether it is worth contributing large amounts of Roth 401(k) contributions, as discussed above. For anyone who is able, I’d always recommend maxing out a Roth IRA.

3. Contribute to a taxable brokerage account.

This was our preferred strategy. For anyone living well within their means and socking away the majority of their income, maxing out a 401(k) and then a Roth IRA won’t be too crazy. The next option is contributing post-tax savings to a brokerage account (we like Vanguard, and I explained how to open a brokerage account with Vanguard in this Q&A post). All past contributions were already taxed, so you are free to spend that money at any point without tax or penalty. Note, however, that all capital gains are taxable. That said, long-term capital gains are taxed very favorably, and any Cap Gain income up to $81,050 in 2021 is 100% tax-free (see chart above).

4. Start a Roth Conversion early.

In theory, one could start doing Roth Conversions five years out before an early retirement, but I don’t see the point unless there simply aren’t funds in a brokerage account. Note, by doing Roth Conversions during working years, a heavier tax burden will likely apply. For high income earners, open yourself a brokerage account now!

Roth Conversion Ladder Summary

The Roth Conversion is the tried-and-true go-to method for accessing retirement money early.

Is this complicated? Hell yeah, dude. It’s complicated.

Is it worth it? Hell yeah, dude. It’s worth it.

While some folks prefer a simpler choice of living off a brokerage account until age 59 ½ —when retirement money can be spent penalty-free—building a sizable brokerage account after maxing out the other up-stream buckets takes a hell of a high income. Even with a portly and healthy brokerage account, it’s still wise to hedge against an unknown future tax code or required minimum distributions (RMD) by moving funds into a tax-free bucket now. I don’t want my traditional IRA funds sitting around waiting to be taxed at a higher tax bracket in the future.

Finally, please note that this is not a strategy to avoid paying taxes entirely. We still pay property taxes, sales tax, and a variety of other state and local taxes. We’re simply lowering income taxes by deliberately lowering income.

What’s your strategy? What do you think of all this converting, jiving, moving, and shaking? We’re having fun over here.

Remember, the best laid plans mean nothing if you can’t take action today. Have questions? Need some feedback? Hit us up on the contact page.

If you enjoyed this post, please subscribe here for much, much more. And please, send this to someone who might enjoy or benefit from this content.

Note that if you have dependent children who qualify for the Child Tax Credit you can convert even more each year. With simple math, 2 kids under 17 are worth $4K in tax credit (plus all the joy and stuff), allowing an additional $40K per year of tax free conversion for a family in the 10% tax bracket.

Plus all the joy and stuff 😂. Thanks for this!

We are using the taxable account method until we turn 59.5. I retired at 45 and my husband worked 5 more years until we were both 50, so we only have to go about 10 years on those accounts. We have them split into a short and a longer term bucket with a heavy bond allocation in the short term bucket. The value of our health care subsidies easily make up for any tax savings. If we fall into the medicaid hole as our interest income drops as the total value of the taxable accounts drop, then we will do some conversions just to keep our MAGI high enough to get a subsidy (we chose a silver plan). This was one of the best summaries of the ROTH conversion that I have seen so far, thanks for the good work!

Thanks for this! I need to chew on your strategy a bit, but it sounds like you guys have given this good thought. So what do you think about RMD on retirement accounts later?

An excellent summary of an excellent strategy.

I’ve been doing something similar for six years. The only difference is that each year I calculate how my conversion to move me as close as I can to the top of the 12% marginal tax bracket, without going over. Some of my conversions are “seasoned,” so I can withdraw them tax free… but I don’t need the money, so I just leave it in the Roth to grow.

I figure, the sooner I can get money out of my traditional and into my Roth, the longer it will have to grow tax free… forever.

Excellent. How do you handle healthcare? We want to go up to the top of the 12% bracket but don’t want to pay higher HC premiums.

Healthcare gives me a bit of indigestion, so I try not to stress about it too much. I just include it in my estimated annual spending. As far as I can figure it, it is almost a wash for Roth Conversions because of Social Security.

Roth IRA conversions are exempt from Social Security and Medicare Tax (7.65% for employee, matched by employer). I view the reduced healthcare premium subsidy as a marginal tax, and it seems to work out to be about 10%.

So, I get to skip 7.65% on Social Security, and have to pay 10% on healthcare, which gives me a net out of pocket of 2.35% vs other types of income. So, every $10k you boost your taxable income, it costs $235, when compared to getting additional income from work… and you don’t have to work to get it!

It’s even better for self employed, because self employment tax rate is 15.3%, so every $10k actually reduces your out of pocket by $530, when compared to taxable self employment income.

I know, this is not an actual opportunity cost because you can both work AND convert a Roth. But, it works for me.

And, it is important to note that we don’t have kids and we are young, so our health insurance premiums are not very expensive anyway. Maybe I will change my answer when we’re 50+ or 60+.

Jay, I really like this way of thinking about it. I’ve been having healthcare indigestion for six months! 😂

Haha – right?! At some point, I realized that I was spending WAY too much time fiddling with something that had WAY too little impact on my overall situation. So, I decided it was time to pick a plan that was “pretty good” instead of “perfect” and move on to higher-return mental activities.

Perfect is the enemy of done, or something. Probably an Einstein quote, like all the rest. 🙂

A very nicely done article with solid details.

So glad to hear, thanks!

Boom! Yeah, I’ve got my Roth conversions starting next year. This year is my first year of “Early Retirement” but have to take all my capital gains to move off of expensive mutual funds. Worth it to better position my portfolio for the long-run.

Yes indeed. I left my job in early 2020, so 2021 will be our first year of conversions. At least LTCG tax rates are forgiving!

Love this and will be adding it to my Fawcett’s Favorites on Monday. One point I would make, you can take your IRA money out before age 59 1/2 without penalty. I have been doing it for years and I’m still not 59 1/2. I wrote a guide about it here: https://financialsuccessmd.com/guide-to-taking-substantially-equal-periodic-payments-sepp-from-your-ira-before-age-59/

Thanks,

Dr. Cory S. Fawcett

Financial Success MD

Yes sir, contributions for sure. Thanks for the feature and the article!

I am digesting your great article. At ages 65 and 69, both retired for 3+ years, these are all things I have been studying and/or implementing in recent years. I wish we had had this information decades ago!

One piece of the puzzle that I want to emphasize is RMD. You do mention it, but it can be a huge factor once you reach that year. It most likely throws you into a higher tax bracket and if so, is a big tax whammy on all of your taxable income. Roth conversions get retirement funds out of government- ruled accounts so that RMDs are not required. This was not on my radar. Luckily, the RMD age was raised to 72.5, and possibly moving higher, so we have more time for conversions.

I really like your charts and your strategy. A point you have made for me is the use of Roth funds after the 5-year “seasoning”.

Question: after retirement and with no wage-earning, the standard recommendation is to keep 2 years of living expenses in cash. This kills me to see that sitting and earning next-to-nothing, but I do agree with the concept of needing it on-hand. Do you have a suggestion or an article for that?

Many thanks!

Hey MM, you are absolutely correct on RMD. I appreciate you doubling down on that message.

I’m with you on cash, although my wife prefers the comfort. Karsten at ERN makes a great convincing argument for no cash here: https://www.google.com/amp/s/earlyretirementnow.com/2016/05/05/emergency-fund/amp/

Interesting strategy that I had not though of before.

I’m glad you enjoyed!

Hey, this is super useful. Thank you.

Question: Say you quit a job, would you recommend converting the associated trad 401k to a trad IRA right then or does it matter (better just wait till closer to retirement)? For context, we’re still a long way (15+ yrs) out from retirement and the trad 401k is in a fidelity account and our main IRA/brokerage accounts are in Vanguard (not clear to me if that matters). Thanks for any insight.

Hi confused, thanks for the kind words!

It really doesn’t matter when you convert a trad 401(k) to a trad IRA (a rollover) after leaving a job. You need to have left the job, of course. But if you are satisfied with the holdings of a previous employer’s 401(k), you can sit on it until you are interested in beginning Roth conversions. I believe you’d want the traditional and Roth IRAs to be held under the same company, but I’m not 100% sure about that.

Just wait to convert trad IRA to Roth IRA in a low tax bracket environment. This will be in the 12% or less tax bracket for many folks.

Wow, you respond with the swiftness! That makes sense. Thanks. I appreciate what you’re doing here. I’m realizing at 31 (after just having a kid) that this personal finance stuff really matters. Who would’ve thought?

You caught me at my desk. Don’t count on that timeliness in all cases! 😉

One more thing to consider: I’ve heard anecdotally that folks with a former employer’s 401(k) had great difficulty rolling it over if that employer was sold or otherwise went out of business, so one reason to roll it soon after leaving.

The early 30s is the magic season for getting into money!

Sure thing, good point.